Does the Plan’s Offerings Meet Your Risk Tolerance?

Target-Date Funds May Not Hit Mark for You

By:July 29, 2021

If you’re investing in a company retirement plan you have likely come across target-date funds. Target-date funds are billed as a one-fund solution for those saving for retirement. They automatically rebalance as you age, becoming more conservative as you get closer to retirement. A “set it and forget it” strategy can be viewed as an attractive solution for investors looking to simply ride the wave of the markets. But that’s not really the point of BetterInvesting and it takes getting under the hood of these funds to understand why there is no one size fits all solution for investors.

Target-date funds are generally defined by four major asset classes: U.S. equities, international equities, U.S. bonds and international bonds. They are constructed as “funds of funds,” which means that each fund is made up of underlying mutual funds. Often, you will notice that a Vanguard Target Date Fund is made up of Vanguard mutual funds, the same with JPMorgan, Charles Schwab and most other target-date fund providers.

Paying attention to the expense ratio, i.e., cost of the fund, is always important and certainly no different with target-date funds. Target-date fund allocations can be created using index funds or managed funds. The index fund variety are often relatively lower in cost, e.g., 0.10%, than those allocated with managed funds, which can have average expense ratios closer to 1.0%. It’s been well documented what those higher expense ratios means for an investor’s net return.

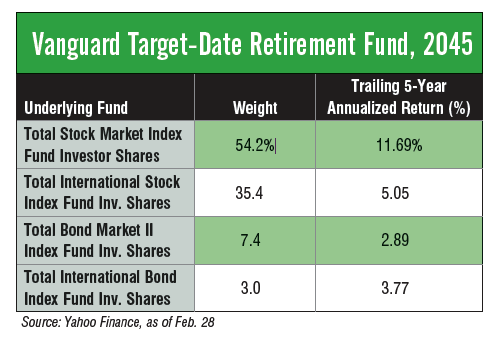

How about the allocation? Assume a 35-year old who wants to retire in 25 years: Using simple math a 35-year old in 2020 anticipating retiring in 25 years can set her retirement contributions to a 2045 target-date fund and forget about it. The Vanguard Target Retirement Fund 2045 (ticker: VTIVX) is made up of four underlying funds allocated in the following percentages, as of March 1, per Vanguard’s website for personal investors (see the below chart).

The stock to bond allocation of the fund in the example was 89.6% (stocks) to 10.4% (bonds). While this allocation may be appropriate for a hypothetical individual, ACTUAL investors have far more to consider than what year they expect to retire. Risk tolerance is an important consideration — not every investor wants to see a portfolio invested 90% in stocks. In fact, finding an allocation that matches your risk tolerance is more effective than simply picking a retirement date.

For complete understanding and transparency, it would be prudent to research each of the underlying funds listed below to understand their weights to various capitalization sizes, home country, sectors, duration of bonds, etc. But, for simplicity’s sake, consider the weight of U.S. stocks (54.2%) versus international stocks (35.2%). The effect of having such a high percentage of the fund allocated towards international stocks has been a significant drag on the portfolio given the relative performance between U.S. equities and international equities. An investor who goes beyond the one-size fits all fund and considers alternative allocations can have a big impact on a portfolio’s return.

For someone looking to put in the time needed to understand how the accounts are being invested, it can pay to go beyond a simple target-date fund. There is a lot to consider, including the alternative options available at your disposal and the cost of investments.

At a minimum, if using a target-date fund, understand how your fund is allocated and determine if that mix is right for you and your financial goals, not just your retirement date.

Disclosures: Expressions of opinion are as of this date and are subject to change without notice. Any information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information has been obtained from sources considered to be reliable, but we do not guarantee that the foregoing material is accurate or complete.

This article was originally published in the May 2020 issue of BetterInvesting Magazine.

Matt Mondoux sits on the investment committee and is anadviser at Blue Chip Partners, Inc., a privately owned,registered investment advisory firm based in Farmington Hills, Michigan.

Visit www.bluechippartners.com.